Although the roots of EBITDA (used as FAVÖK in Turkey) date back to the late 1970s, it has become one of the most debated financial indicators in the business world in recent years. Once regarded as the "must-have" metric for bosses, CEOs, and investors, EBITDA is now being questioned as to whether it is a sufficient measure on its own.

The main point of criticism is that it excludes borrowing costs, tax burdens, and the real impact on cash flow. For this reason, many managers and experts argue that EBITDA is only meaningful when considered alongside indicators such as net profit and free cash flow.

The concept of EBITDA was developed in the late 1970s by American businessman and Tele-Communications CEO John Malone. The aim was to create a metric that could more clearly show the operational performance of companies growing with high debt. This approach, which bypasses taxes, interest, and non-cash expenses, became attractive to investors, especially during periods of leveraged growth. Since the 1980s, EBITDA has spread rapidly and played a central role in company valuations for many years.

One of the harshest criticisms of EBITDA came from Warren Buffett. The founder of Berkshire Hathaway argued that EBITDA is used to "dress up" financial statements and openly stated that they do not invest in companies that prioritize this metric. While not as severe as Buffett’s approach, many CEOs and finance managers today agree that EBITDA is a limited indicator.

The CEO of Diageo Turkey emphasizes that while EBITDA is useful for evaluating operational performance, it is not sufficient on its own:

"EBITDA is a good indicator for operational performance evaluation. However, it does not fully reflect financial health because it excludes borrowing costs, tax obligations, and the impact on cash flow."

According to the CEO, for a healthy performance reading, revenue growth, profitability increase, and positive cash flow must be evaluated together. Additionally, indicators such as employee engagement, ecosystem health, and stakeholder satisfaction are closely monitored.

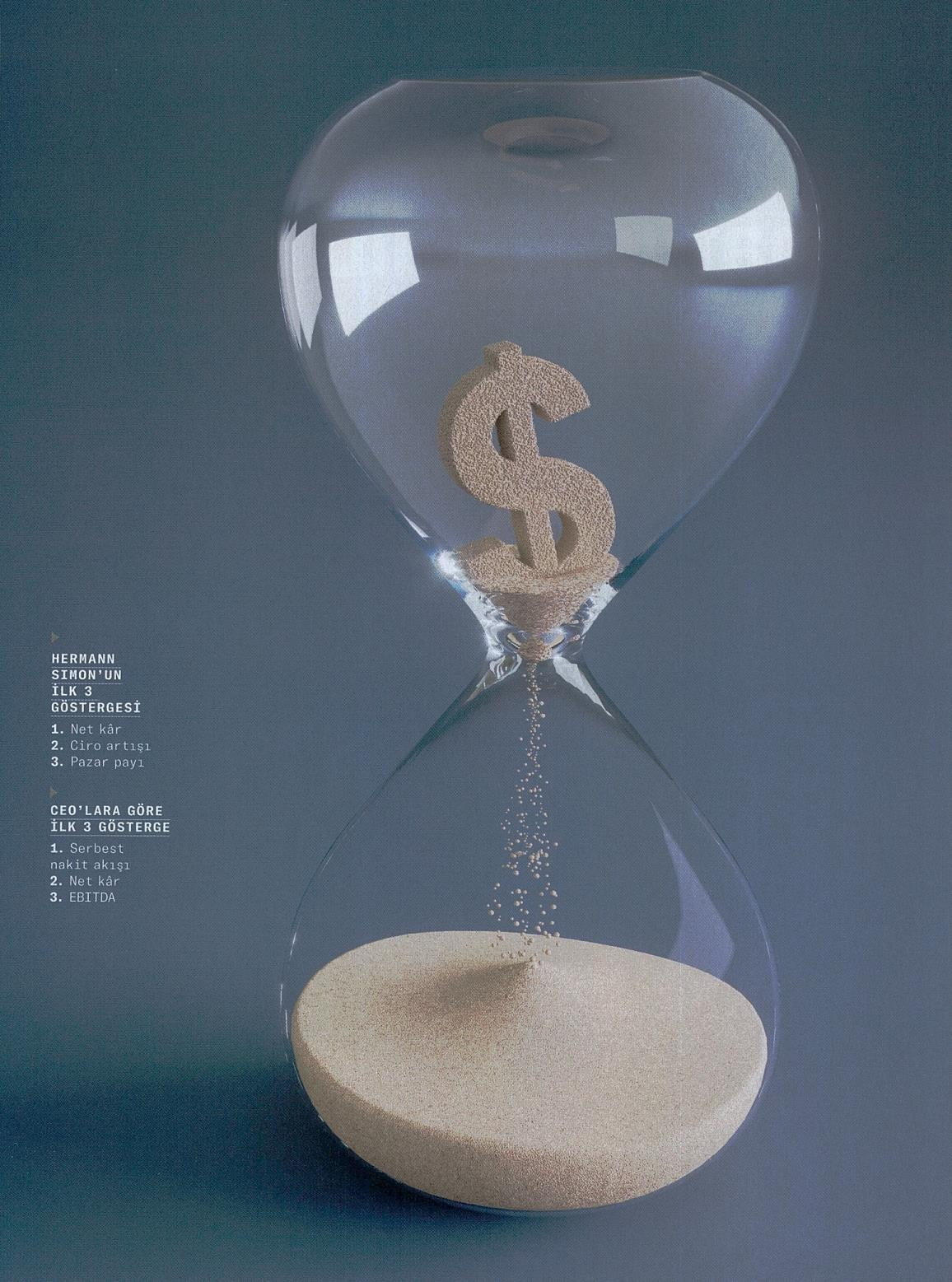

İhsan Erbil Bayçöl, CEO of Enerjisa Üretim, points out the risk of focusing on a single financial indicator. Emphasizing that they make decisions using scenario-based projections and multiple metrics, Bayçöl says he does not agree with the "number one indicator" philosophy. A similar view is shared by Hermann Simon, author of Hidden Champions, who believes "the number one indicator is net profit."

Academic and corporate research also supports this view. According to an analysis by the American Bankruptcy Institute, one-third of companies entering bankruptcy protection programs had positive EBITDA values before entering the program. However, the free cash flows of these companies had turned negative. This picture reveals that EBITDA alone cannot reflect a company's true financial resilience.

The general trend in the business world is not to exclude EBITDA entirely, but to evaluate it alongside indicators such as cash flow, net profit, share value, customer data, and sustainability.

- Ozan Diren (CEO, Dimes): Emphasizes that measuring success solely with financial metrics is no longer enough: "We read sustainable profitability alongside innovation, producer trust, and consumer loyalty."

- Şükrü Bekdikhan (CEO, Mercedes-Benz Turkey): Draws attention to value-oriented growth, stating that it encompasses not only financial profitability but also customer satisfaction and sustainability.

EBITDA is still an important indicator. However, the view increasingly accepted in the business world is: It is not "Number 1" on its own.

EBITDA-focused evaluations made without considering the company's stage, industry dynamics, and economic conditions can lead to misleading results. Therefore, financial success is now measured not by a single figure, but through a multi-dimensional perspective.